“True expert knowledge in life and investing does not exist, only varying degrees of ignorance.”

Gautam Baid

Arrogance means having strong headwind ahead: being arrogant means to close our minds to alternative ways of seeing the world, while being humble means to be open to new ideas and visions.

Why?

Because nobody has such an extensive knowledge that allows to discart any new input, not even on a single specific niche of the knowledgeable universe. This is due to the fact that knowledge is immense: even if we master a specific area of knowledge (for example: equity investing or bioinformatics) we know that there are some topics within this area that we do not know; in addition there are possibly topics that we do not know that exist and they may represent a relevant piece of the knowledgeable universe!

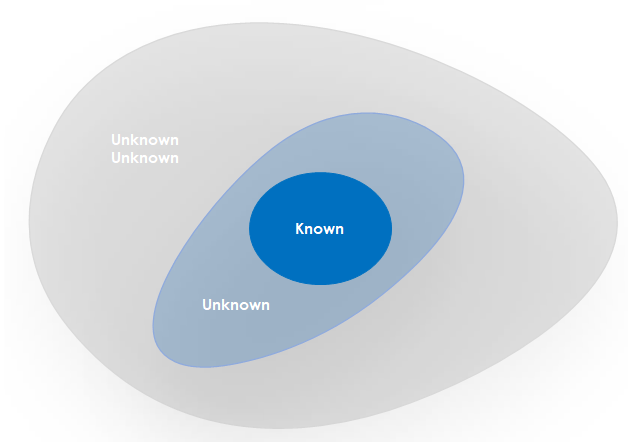

In summary we should always be aware that, out of a certain knowledge universe:

- We know something (KNOWN)

- We know that there is something that we do not know (UNKNOWN)

- There is a last area of knowledge that we are not aware of (UNKNOWN UNKNOWN), which could likely cover most of the knowledge universe!

Being aware about our limitations may be a very powerful way of counteract the Dunning-Kruger effect, which is a cognitive bias whereby people with low expertise and knowledge regarding a specific universe of knowledge overestimate their knowledge.

Having in mind this, we can act being humble in front of new pieces of information and new opinions that come from other people.

Being open minded and accepting that the person in front of us may be right even if in contrast with our beliefs and knowledge is a great cognitive advantage.

Therefore be humble, not arrogant.